All,

Effective today, I'm going with the following allocations:

C-Fund: 0%

F-Fund: 14%

G-Fund: 76%

I-Fund: 0%

S-Fund: 10%

I will make the change prior to lunch today so that it is effective at the end of the day.

Regards,

pgd

Friday, December 30, 2011

Wednesday, November 30, 2011

TSP Change Effective November 30th

.

All,

I’m updating my TSP allocation to the following:

G-Fund: 59%

F-Fund: 18%

C-Fund: 11%

S-Fund: 10%

I-Fund: 2%

If you make your changes by noon EDT they will be effective today. If you wait a day, no issues in the big picture, except the exchange will count against the two you have available in December.

The rationale for the change today is partly based on numbers and partly based on seasonality. The numbers part is due to a number of my short-term timers indicating that we have been oversold and that we need to participate in the present climate. The move over the last few days has been quite weak though, and I expect more of the same, hence why 59% is in cash.

The seasonality component typically says that the period between Thanksgiving and Christmas has been up more than it has been down. We have had no exposure to equities, hence the move into the C-Fund (11%), S-Fund (10%), and I-Fund (2%). Our risk is quite controlled here and if this signal reverses (very possible), we'll move back into cash/bonds.

Regards,

pgd

Monday, October 17, 2011

Allocation Change for Monday, October 17

Effective immediately, I’m changing TSP allocations:

G-Fund: 94%

F-Fund: 6%

My short-term risk model has signaled overbought conditions and stalling, which is where we are not advancing yet we are exposed in terms of risk. Even with the significant strength in the I-Fund and C-Funds, I’m anticipating a short-term pullback which will reveal itself to be either shallow (a buying opportunity) or worse-than-previous (“thank gosh we moved to cash and bonds”). I expect to be making another allocation change within the next few weeks, depending upon the anticipated pullback. If we continue higher with no pullback, risk dominates from here and upside is quite limited compared to how far we can fall.

If you make the change prior to 12:00 EDT the change will be effective today.

As a reference point, since our allocation on 8/31/11, we are nearly EVEN on the market, specifically, down only -0.087%. No gain in this time frame and some exposure is not a good situation, hence the need for the reallocation.

In reality, for the period 8/31/11 to 10/14/11, the previous allocations have resulted in the following gains and (unrealized) drawdowns:

G-Fund: +0.149% gain, no drawdown

F-Fund: -0.011% gain, -0.028% maximum drawdown

C-Fund: +0.041% gain, -0.545% MDD

S-Fund: -0.128% gain, -0.959% MDD

I-Fund: -0.138% gain, -0.727% MDD

Totals: -0.087% gain, -1.927% MDD

For the past 12 month rolling period, we are up 6.94% with -3.325% realized drawdown (May 24th). This is a 2:1 reward : risk ratio and is our minimum goal.

For the past 12 month rolling period, we are up 6.94% with -3.325% realized drawdown (May 24th). This is a 2:1 reward : risk ratio and is our minimum goal.

Cash is king, at least for the next week or two.

Regards,

pgd

Monday, September 5, 2011

Weekend Update for September 2nd

.

Changes to the account were made on August 31st in accordance with the previous post. Since that time we've lost -0.574% in the account with the broader markets losing between -2.8% and -4.5%, but on a rolling-year basis we're up nearly +10.35%, so we're doing well. The aggressive strategies that I use in my wife's TSP account showed that August was a good month for us, where we caught +2.9% gain with only about 1/3 exposure to the markets. Note that over this time frame the S&P500 lost a bit more than 5% and drawdown was considerably more.

Looking forward to the next few weeks, your crystal ball is as good as mine. This being said, the following document gives you some perspective on the market from an professional view. Pay particular attention to the comments about the SPX falling through 1100 and ultimately testing as low as 1018, which will certainly cause me to move all our equity exposure to cash as soon as 1100 is penetrated. Conversely, if 1100 is tested and holds, then I'll more than likely become more bullish and expose a bit more to the equity side of the markets.

To recap, we're 79% in the G-Fund (money markets), 12% in the F-Fund (bonds), 5% in the C-Fund (S&P500), 3% in the S-Fund (ex-S&P500), and 1% in the I-Fund (international). I'm holding this allocation into the upcoming week.

=================

Remember, you are responsible for your own trading, and I am not. Please do your diligence, and please take ownership for your actions.

Regards,

pgd

Changes to the account were made on August 31st in accordance with the previous post. Since that time we've lost -0.574% in the account with the broader markets losing between -2.8% and -4.5%, but on a rolling-year basis we're up nearly +10.35%, so we're doing well. The aggressive strategies that I use in my wife's TSP account showed that August was a good month for us, where we caught +2.9% gain with only about 1/3 exposure to the markets. Note that over this time frame the S&P500 lost a bit more than 5% and drawdown was considerably more.

Looking forward to the next few weeks, your crystal ball is as good as mine. This being said, the following document gives you some perspective on the market from an professional view. Pay particular attention to the comments about the SPX falling through 1100 and ultimately testing as low as 1018, which will certainly cause me to move all our equity exposure to cash as soon as 1100 is penetrated. Conversely, if 1100 is tested and holds, then I'll more than likely become more bullish and expose a bit more to the equity side of the markets.

To recap, we're 79% in the G-Fund (money markets), 12% in the F-Fund (bonds), 5% in the C-Fund (S&P500), 3% in the S-Fund (ex-S&P500), and 1% in the I-Fund (international). I'm holding this allocation into the upcoming week.

=================

Remember, you are responsible for your own trading, and I am not. Please do your diligence, and please take ownership for your actions.

Regards,

pgd

Wednesday, August 31, 2011

End-of-August Update/Tweak

.

I am updating this as we move into the last day of August.

Over the last week the rate-of-change indicators on the C-Fund (SPY), I-Fund (EFA), and S-Fund (VXF) have moved quickly -- too quickly in fact. I am aggressively allocated as per my previous message here, and the gains since that change are +1.203% in 6 trading days. Normally, I'd yawn at this, but considering that we're heavily in cash (G-fund, 67%), this is a notable movement and one that is too aggressive for the volatility of the markets right now.

My risk models are all suggesting that this leg upward is failing to materialize, and that we are due for a pullback. While my longer-termed outlook is still cloudy (your crystal ball is as good as mine), my short-termed one suggests a reallocation to lighten up on equity until we get a clearer emergence of a trend upward.

Again, this trend upward has moved far too fast to be sustained. Given this, I'm moving my wife's funds around as follows:

G-Fund: 79%

F-Fund: 12%

C-Fund: 5%

S-Fund: 3%

I-Fund: 1%

I consider this quasi-aggressive/conservative. If your time horizon is long (like mine -- about 9 years), then this is probably too conservative, but I feel better. Conversely, if your time horizon is short (e.g., less than 1-2 years), then for the short-term future (next month or so), then this allocation is probably a little too aggressive in the present climate. If you fall into the shorter-termed category, look to lighten up (0% in) the I-Fund and S-Fund and put these monies into the G-Fund as a temporary parking place. Both the S-Fund (small cap stocks) and the I-Fund (international stocks) are getting the heck walloped out of them lately and have the highest volatility. A 20% drop in the markets here with the allocations shown above would take 2% off the top, and we've fought hard for these gains over the past 8 months (over 7% on a rolling 12 month tally).

Recapping, if conservative, look to the following allocation:

G-Fund: 83%

F-Fund: 12%

C-Fund: 5%

================

Remember, you are responsible for your own investment decisions, and I am not. Please do your diligence, and please take ownership for your actions.

We'll revisit the portfolio this weekend.

Regards,

pgd

I am updating this as we move into the last day of August.

Over the last week the rate-of-change indicators on the C-Fund (SPY), I-Fund (EFA), and S-Fund (VXF) have moved quickly -- too quickly in fact. I am aggressively allocated as per my previous message here, and the gains since that change are +1.203% in 6 trading days. Normally, I'd yawn at this, but considering that we're heavily in cash (G-fund, 67%), this is a notable movement and one that is too aggressive for the volatility of the markets right now.

My risk models are all suggesting that this leg upward is failing to materialize, and that we are due for a pullback. While my longer-termed outlook is still cloudy (your crystal ball is as good as mine), my short-termed one suggests a reallocation to lighten up on equity until we get a clearer emergence of a trend upward.

Again, this trend upward has moved far too fast to be sustained. Given this, I'm moving my wife's funds around as follows:

G-Fund: 79%

F-Fund: 12%

C-Fund: 5%

S-Fund: 3%

I-Fund: 1%

I consider this quasi-aggressive/conservative. If your time horizon is long (like mine -- about 9 years), then this is probably too conservative, but I feel better. Conversely, if your time horizon is short (e.g., less than 1-2 years), then for the short-term future (next month or so), then this allocation is probably a little too aggressive in the present climate. If you fall into the shorter-termed category, look to lighten up (0% in) the I-Fund and S-Fund and put these monies into the G-Fund as a temporary parking place. Both the S-Fund (small cap stocks) and the I-Fund (international stocks) are getting the heck walloped out of them lately and have the highest volatility. A 20% drop in the markets here with the allocations shown above would take 2% off the top, and we've fought hard for these gains over the past 8 months (over 7% on a rolling 12 month tally).

Recapping, if conservative, look to the following allocation:

G-Fund: 83%

F-Fund: 12%

C-Fund: 5%

================

Remember, you are responsible for your own investment decisions, and I am not. Please do your diligence, and please take ownership for your actions.

We'll revisit the portfolio this weekend.

Regards,

pgd

Monday, August 22, 2011

August 21st Weekend Update

.

In a nut shell -- no changes unless you have some tolerance for risk.

==============

I am presently 54% in the G-Fund (the equivalent of a money market) and 46% in the F-Fund (the equivalent of a bond fund). Since these allocations on June 6:

In a nut shell -- no changes unless you have some tolerance for risk.

==============

I am presently 54% in the G-Fund (the equivalent of a money market) and 46% in the F-Fund (the equivalent of a bond fund). Since these allocations on June 6:

- F-Fund increase 3.218%

- G-Fund increase 0.511%

In the same time the equity funds have been slammed:

- C-Fund (equivalent to S&P500): -12.090%

- I-Fund (equivalent to international index): -15.732%

- S-Fund (equivalent to ex-S&P500): -16.787%

The allocations above in the account have a net realized and unrealized gain of +1.756% over 54 days, with the drawdown never exceeding -0.173%. Drawdown is what makes us nervous and will take us off course with our strategies, so I'm comfortable with the present allocations.

==================

Outlook:

We may see some pressure on bonds (F-Fund) if the market begins to rally from here. We are forming the second "bounce" of a double dip this summer, and the right side of a "W" typically keeps on moving upward if conditions are correct. We literally are at the bottom of the second dip, so there is nothing to do in terms of allocations unless you are aggressive in your tolerance for risk. My preferred approach here is to wait until we get an "all clear" on the equity markets (C-Fund, I-Fund, S-Fund), and as of today they are all quite bearish and telling us to sit on the sidelines.

No one would fault you if you took the F-Fund down to low values in your allocation, effectively locking in your gains to date.

No one would fault you if you also moved some funds into the equities, although this is a risky proposition at this time and could easily backfire. For those of you interested in representative allocations, here are some suggestions:

- F-Fund (bonds): 14%

- I-Fund (international): 6%

- C-Fund (S&P500): 6%

- S-Fund (ex-S&P500): 7%

- G-Fund (money mkt): 66%

Because my time horizon is longer, I plan to make the allocation changes above, effective today. If you have a shorter time horizon than myself, I would consider sitting pat for now.

===================

Remember, you are responsible for your own investment decisions, and I am not. Please do your own diligence, and please take ownership for your actions.

Regards,

pgd

Sunday, August 7, 2011

August 7 Weekend Update

.

I'm presently 54% in G-Fund, which is the equivalent of a money-market cash fund, and the balance is in the F-Fund, which is a bond fund. We made this move effective June 6, 2011.

Since June 6 the account has increased +1.105% using the allocation levels above. The high point of +1.365% was achieved with the close of markets on 8/4, and the low point of -0.173% was achieved on 7/1. Given recent markets, this allocation is allowing me to sleep quite well and not have to play with this portfolio at all.

For the rolling 12-month period ending 7/31 the account has returned +6.36%. This value has been dropping over the past several months due to the cash position, but I do not think it is dropping as fast as it would have if we were in equities (C-Fund, I-Fund, S-Fund).

In the same time the performance of the individual funds is as follows:

I'm presently 54% in G-Fund, which is the equivalent of a money-market cash fund, and the balance is in the F-Fund, which is a bond fund. We made this move effective June 6, 2011.

Since June 6 the account has increased +1.105% using the allocation levels above. The high point of +1.365% was achieved with the close of markets on 8/4, and the low point of -0.173% was achieved on 7/1. Given recent markets, this allocation is allowing me to sleep quite well and not have to play with this portfolio at all.

For the rolling 12-month period ending 7/31 the account has returned +6.36%. This value has been dropping over the past several months due to the cash position, but I do not think it is dropping as fast as it would have if we were in equities (C-Fund, I-Fund, S-Fund).

In the same time the performance of the individual funds is as follows:

- S&P500/C-Fund has returned +14.68% with a drawdown of -7.04%

- F-Fund has returned +0.68% with a drawdown of -4.63%

- I-Fund has returned +9.51% with a drawdown of -10.7%

- S-Fund has returned +22.43% with a drawdown of -8.88%

For comparisons, a buy/hold with equal weight on 8/2/10 within the equity funds (C, I, S) would have produced a return of +15.49% with a drawdown of -8.01%.

====================

While I am somewhat disappointed at the returns compared to the benchmarks above I am quite content with the recent performance. My longer-termed models have been quite bearish and hence the move in June.

The C-Fund has fallen -11.28% in the last month. The I-Fund has fallen the same amount. The S-Fund has dropped -16.55%. Standard & Poors downgraded the debt rating of the U.S. after the market close on Friday night, in order to give the pundits time to think about this over the weekend.

Now is not the time to be in equities. Although I do like to buy 20% of the recommended position size in equities with every drop of 10%, I'm going to hold off on this rule for now. Despite this, for those of you who are more aggressive, you could allocate as follows:

F-Fund: 59%

C-Fund: 4%

I-Fund: 4%

S-Fund: 1%

G-Fund: 32%

This could be a good allocation if you have a long-term horizon, as it will permit you to participate on the upside if we move upward from here. Conversely, if the markets fall, your exposure to the general markets is limited, even if they drop 25% from here (25% of 4 is 1%, so the most at risk is ~ 3%).

If the markets continue to drop I will most likely move some funds into equities as we cross the -20% from the peak level.

========================

Remember, you are responsible for your own investment decisions, and I am not. Please do your diligence and please take ownership for your actions.

Regards,

pgd

Friday, July 8, 2011

Friday, July 8th Update

.

I'm sure many of you are wondering if the TSP allocations are going to flip any time soon, as the markets are up substantially in the last week or so.

Before we get there, let's review a couple of key points:

1) we can only move 2x within a given month.

2) historically, summer rallies are suspect, and are quite often fickle, as they can change quickly. This can quickly unravel any unrealized gains that we have attained.

With this backdrop, let's look at the relevant timers:

Right click on the image to open in a separate window or browser tab.

This first one is the GGT set of timers that I use on proxy ETFs. Here:

AGG = F-Fund

EFA = I-Fund

SPY = C-Fund

VXF = S-Fund

This set of timers uses price and volume to move long, and only price to move to cash.

You can see that the recommendations of the GGT system point us towards:

AGG / F-Fund in CASH

EFA / I-Fund invested LONG

SPY / C-Fund in CASH

VXF / S-Fund invested LONG

Quite a mixed bag. What is best is when these are confirming, e.g., AGG is CASH (as now) and the others are all LONG (SPY is the holdout). We do NOT have confirmation of this bull leg according to this timing system.

=============

We can group the three equity trades into a basket to form an index. When the 5d simple moving average crosses the 65d SMA from below, we have a general buy signal for the three equities. When the 5d crosses the SMA from above, we have a general sell signal.

This method is confirmed by the slope of the 65d SMA -- when it is positive, we have confirmation. When it is negative, we avoid long positions.

This method avoids volume considerations.

Here's the chart:

The top pane is the slope of the 65d simple moving average. You can see that it is positive, which is bullish. You can also see that it is trending SIDEWAYS, e.g., not moving up. This is cautionary.

You can see in the next lower pane that the 5d crossed the 65d from below. In general this is a good indication, and is confirmed with the slope of the 65d above.

Finally, we see that in the pricing pane that price has started to trade above the 65d MA. While not on a upward trajectory, the repeated close above the 65d for the past 4 days is encouraging.

From this chart, we can conclude that we have a confirmed entry on the 3 equity positions: I-Fund, S-Fund, and C-Fund.

====================

Before we get all excited, I think it's important to understand the money flow into each of these ETFs. Note that this is for the ETFs, NOT the individual funds (C-Fund, I-Fund, F-Fund, S-Fund). The importance here is that the market plays these ETFs just like we are playing the TSP funds, so it's a reasonable proxy to be able to look at each of these ETFs in terms of money flow.

You can do this work yourself by joining the Effective Volume group at http://forums.effectivevolume.com

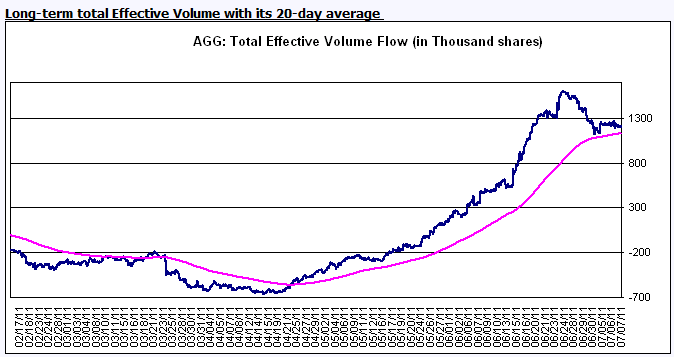

Here's AGG / F-Fund:

You're looking at what the large players are doing with AGG, which is a bond fund. The blue trace is total effective volume (TEV), and the purple trace is a 20d moving average.

I look for the 20d MA to be pointing upward for a confirmation that I should be in the equity. As you can see, AGG is still attracting money, but is doing it less fast than a few weeks ago. If the TEV line crosses below the 20d MA then institutional support for AGG is declining, which is a bigger problem. In general, I would not abandon AGG / F-Fund, simply because the 20d TEV line is still pointing upwards.

Next is the EFA / I-Fund:

Here, you can see that the 20d TEV line is in a strong uptrend, and that daily TEV continues to pull this line upward rather aggressively. EFA / I-Fund appears to have significant institutional support, although you can see that over the past few months it has been very, very choppy. This is somewhat problematic for our time horizon, but nevertheless, right now EFA appears to have the required sponsorship.

Next is the SPY / C-Fund:

The SPY is one of the most liquid (traded) ETFs on the market, so the TEV values above are quite relevant. You can see that the 20d TEV levels are in a significant uptrend, and appears very strong. Institutional support for the SPY is very strong.

Finally, the VXF / S-Fund is the last ETF to consider:

The presentation changed because the Effective Volume site does not track VXF, which is not nearly as liquid as the other ETFs.

The yellow and blue traces above are the relevant TEV and Large EV traces for VXF respectively, over the past week or so. The nearly-horizontal red trace shows that Small EV folks (you and I) are not moving aggressively into VXF as an instrument. The positive divergence of the TEV for VXF does point to significant institutional support, so I am encouraged.

Conclusion: EFA has choppy TEV patterns, which means institutional support is mixed and fickle. AGG, SPY, and VXF all look relatively good in terms of institutional support.

=====================

Given these conditions, the last decision is whether to jump in today, Friday, or wait for a pullback.

I prefer to wait for a pullback. As long as the TEV 20d lines remain in an uptrend, we're relatively safe. As long as the TEV continues to trade above the 20d lines, we have institutional support. The overall problem is that the markets are heavily overbought, and there has not been a good opportunity to get into this rally except just to plunge in. I do not "plunge", so I'm going to wait for the inevitable pullback.

For those of you who are aggressive, you can go with the following allocations:

AGG / F-Fund: 6%

EFA / I-Fund: 10%

SPY / C-Fund: 38%

VXF / S-Fund: 46%

This allocation will take advantage of the recent momentum but understand, it is a very aggressive stance.

=========================

The maximum gain/minimum volatility play is 100% in the VXF / S-Fund. It is not unreasonable to expect an incredible amount of volatility here (~ 17%), but of the 4 funds, this has the largest potential gains going forward.

========================

The minimum volatility play, if you are not convinced in this market action, is as follows:

AGG / F-Fund: 87%

EFA / I-Fund: 2%

SPY / C-Fund: 10%

VXF / S-Fund: 1%

If we see a pullback I expect that AGG will perform quite well, relative to the other securities. Conversely, if we continue upwards, this portfolio mix will significantly underperform the markets.

=====================

Uncertain times. You'll have to choose the portfolio mixture that is aligned with your tolerance for drawdown and volatility.

I personally am going to wait for a pullback in the markets before changing my allocation, which is heavily weighted in the F-Fund.

====================

I'm sure many of you are wondering if the TSP allocations are going to flip any time soon, as the markets are up substantially in the last week or so.

Before we get there, let's review a couple of key points:

1) we can only move 2x within a given month.

2) historically, summer rallies are suspect, and are quite often fickle, as they can change quickly. This can quickly unravel any unrealized gains that we have attained.

With this backdrop, let's look at the relevant timers:

Right click on the image to open in a separate window or browser tab.

This first one is the GGT set of timers that I use on proxy ETFs. Here:

AGG = F-Fund

EFA = I-Fund

SPY = C-Fund

VXF = S-Fund

This set of timers uses price and volume to move long, and only price to move to cash.

You can see that the recommendations of the GGT system point us towards:

AGG / F-Fund in CASH

EFA / I-Fund invested LONG

SPY / C-Fund in CASH

VXF / S-Fund invested LONG

Quite a mixed bag. What is best is when these are confirming, e.g., AGG is CASH (as now) and the others are all LONG (SPY is the holdout). We do NOT have confirmation of this bull leg according to this timing system.

=============

We can group the three equity trades into a basket to form an index. When the 5d simple moving average crosses the 65d SMA from below, we have a general buy signal for the three equities. When the 5d crosses the SMA from above, we have a general sell signal.

This method is confirmed by the slope of the 65d SMA -- when it is positive, we have confirmation. When it is negative, we avoid long positions.

This method avoids volume considerations.

Here's the chart:

The top pane is the slope of the 65d simple moving average. You can see that it is positive, which is bullish. You can also see that it is trending SIDEWAYS, e.g., not moving up. This is cautionary.

You can see in the next lower pane that the 5d crossed the 65d from below. In general this is a good indication, and is confirmed with the slope of the 65d above.

Finally, we see that in the pricing pane that price has started to trade above the 65d MA. While not on a upward trajectory, the repeated close above the 65d for the past 4 days is encouraging.

From this chart, we can conclude that we have a confirmed entry on the 3 equity positions: I-Fund, S-Fund, and C-Fund.

====================

Before we get all excited, I think it's important to understand the money flow into each of these ETFs. Note that this is for the ETFs, NOT the individual funds (C-Fund, I-Fund, F-Fund, S-Fund). The importance here is that the market plays these ETFs just like we are playing the TSP funds, so it's a reasonable proxy to be able to look at each of these ETFs in terms of money flow.

You can do this work yourself by joining the Effective Volume group at http://forums.effectivevolume.com

Here's AGG / F-Fund:

You're looking at what the large players are doing with AGG, which is a bond fund. The blue trace is total effective volume (TEV), and the purple trace is a 20d moving average.

I look for the 20d MA to be pointing upward for a confirmation that I should be in the equity. As you can see, AGG is still attracting money, but is doing it less fast than a few weeks ago. If the TEV line crosses below the 20d MA then institutional support for AGG is declining, which is a bigger problem. In general, I would not abandon AGG / F-Fund, simply because the 20d TEV line is still pointing upwards.

Next is the EFA / I-Fund:

Here, you can see that the 20d TEV line is in a strong uptrend, and that daily TEV continues to pull this line upward rather aggressively. EFA / I-Fund appears to have significant institutional support, although you can see that over the past few months it has been very, very choppy. This is somewhat problematic for our time horizon, but nevertheless, right now EFA appears to have the required sponsorship.

Next is the SPY / C-Fund:

The SPY is one of the most liquid (traded) ETFs on the market, so the TEV values above are quite relevant. You can see that the 20d TEV levels are in a significant uptrend, and appears very strong. Institutional support for the SPY is very strong.

Finally, the VXF / S-Fund is the last ETF to consider:

The presentation changed because the Effective Volume site does not track VXF, which is not nearly as liquid as the other ETFs.

The yellow and blue traces above are the relevant TEV and Large EV traces for VXF respectively, over the past week or so. The nearly-horizontal red trace shows that Small EV folks (you and I) are not moving aggressively into VXF as an instrument. The positive divergence of the TEV for VXF does point to significant institutional support, so I am encouraged.

Conclusion: EFA has choppy TEV patterns, which means institutional support is mixed and fickle. AGG, SPY, and VXF all look relatively good in terms of institutional support.

=====================

Given these conditions, the last decision is whether to jump in today, Friday, or wait for a pullback.

I prefer to wait for a pullback. As long as the TEV 20d lines remain in an uptrend, we're relatively safe. As long as the TEV continues to trade above the 20d lines, we have institutional support. The overall problem is that the markets are heavily overbought, and there has not been a good opportunity to get into this rally except just to plunge in. I do not "plunge", so I'm going to wait for the inevitable pullback.

For those of you who are aggressive, you can go with the following allocations:

AGG / F-Fund: 6%

EFA / I-Fund: 10%

SPY / C-Fund: 38%

VXF / S-Fund: 46%

This allocation will take advantage of the recent momentum but understand, it is a very aggressive stance.

=========================

The maximum gain/minimum volatility play is 100% in the VXF / S-Fund. It is not unreasonable to expect an incredible amount of volatility here (~ 17%), but of the 4 funds, this has the largest potential gains going forward.

========================

The minimum volatility play, if you are not convinced in this market action, is as follows:

AGG / F-Fund: 87%

EFA / I-Fund: 2%

SPY / C-Fund: 10%

VXF / S-Fund: 1%

If we see a pullback I expect that AGG will perform quite well, relative to the other securities. Conversely, if we continue upwards, this portfolio mix will significantly underperform the markets.

=====================

Uncertain times. You'll have to choose the portfolio mixture that is aligned with your tolerance for drawdown and volatility.

I personally am going to wait for a pullback in the markets before changing my allocation, which is heavily weighted in the F-Fund.

====================

Tuesday, June 28, 2011

End of June Preparation

.

In a nutshell, I am making no changes to my wife's TSP account. The allocation in F-Fund remains at 46% and the allocation in the G-Fund remains at 54%.

==================

The past two days have not been kind to the TSP -- we've lost all of the gains of the month due to a plummeting bond market/rising equity market these past two days, which directly impacts the F-Fund. We are presently even (-0.03%) since our last signal to move into the F-Fund.

Despite the short-term strength in the equity markets, I cannot see any compelling reason to jump into the equity funds for the longer haul. This may change if we continue to see strength in the equity markets AFTER July 4, so our next bogey will be the week of July 4-8, when QE2 ends and Wall Street comes back from vacation.

Earnings season is upon us, and this could compel us to move into equities.

I intend to let the indicators do their job, rather than try to anticipate a bump at this time.

Regards,

pgd

In a nutshell, I am making no changes to my wife's TSP account. The allocation in F-Fund remains at 46% and the allocation in the G-Fund remains at 54%.

==================

The past two days have not been kind to the TSP -- we've lost all of the gains of the month due to a plummeting bond market/rising equity market these past two days, which directly impacts the F-Fund. We are presently even (-0.03%) since our last signal to move into the F-Fund.

Despite the short-term strength in the equity markets, I cannot see any compelling reason to jump into the equity funds for the longer haul. This may change if we continue to see strength in the equity markets AFTER July 4, so our next bogey will be the week of July 4-8, when QE2 ends and Wall Street comes back from vacation.

Earnings season is upon us, and this could compel us to move into equities.

I intend to let the indicators do their job, rather than try to anticipate a bump at this time.

Regards,

pgd

Saturday, June 25, 2011

Weekend Update for June 24th

The risk model that I use is still quite bearish; there are a number of indicators that are in pretty bad shape so I don't think that we'll be going long any time soon. We may rebalance at the end of the month, and if we continue south, we may move some of our capital to equity funds.

C-Fund

The C-Fund is designed to mimic the S&P500; here's the latest chart ( as with all my charts, right click on the image to open in a new window or tab):

This chart is interesting for a couple of reasons:

C-Fund

The C-Fund is designed to mimic the S&P500; here's the latest chart ( as with all my charts, right click on the image to open in a new window or tab):

This chart is interesting for a couple of reasons:

- The S&P500 has tested the 200d simple moving average (MA) twice intra day within the past two weeks, and has closed above it each time. The 200d MA is the RED line. The test is damaging if no recovery occurs, but the close above is bullish in general. A penetration of the 200d MA and a subsequent close below it would be problematic -- although there is a weak support level shown by the shorter, horizontal blue line, which sits at 1249.05.

- If 1249 does not hold, it's Katie, bar the doors. The next program support level most likely would be around 1173, which is another -7% below where we are presently.

- The downward green line is the lower channel line formed by multiple touch points as the S&P500 has fallen. If the 200d MA does not hold, I would expect that the falling trajectory would be aligned with this downward sloping line.

- The horizontal yellow line is a weak resistance line, formed recently by two tests within the past two weeks, and slightly penetrated this past week. For the bulls to be back in control, we need a close above this level, as no floor has yet been established.

- The 50d MA (blue) and 20d MA (green) are above the price and are converging towards the 200d MA. This squeeze has to be resolved one way or another -- in general, prices do not like to remain in this squeeze pattern. Either the prices will drop below the 200, pulling everything down, or a new bull will (aggressively) take the prices up, testing the 20d and the 50d.

In all, my GGT timing system has multiple timers indicating that we should NOT be holding the C-Fund; if you are, you are taking on a considerable amount of risk for uncertain gain potential at the present moment.

===========================

F-Fund

The F-Fund is a bond fund. Typically, I prefer not to be "in" a bond fund, as it simply takes away from all the other capital available for the equity funds, which is true when equity is rising. Right now, equity is falling, so bonds and cash make sense.

I think we're in 46% in this fund, which is a large amount of our allowed capital percentage. The ETF that is a proxy for the F-Fund is the AGG; the chart continues to look good:

What should catch your eye is the following:

- We're still above the green 20d MA, although we saw some weakness over the past two weeks. The fact that we recovered above the 20d MA suggests we should stay the course.

- The 20d MA, as well as the 50d MA, are pointing upward (positive slope). On these time frames the F-Fund is making money.

- The 50d is above the 200d MA, which occured on 6/16. I anticipated this, but it took longer than I thought, but this is why I suggested moving long into the F-Fund the on June 6th.

I see no reason that we should not continue our position in the F-Fund for the immediate future. Note that we may rebalance this amount on June 29th or June 30th; we'll see. Put it on your calendar to check in with this blog.

======================

I-Fund

The I-Fund tracks the MSCI European Asian Far Eastern (EAFE) index, and the proxy for this index is the ETF called EFA. This index is broken, and you should NOT be holding any funds in the I-Fund at the present time. Here's the chart:

Unlike the C-Fund / S&P500 chart, there are numerous potential points for support within the I-Fund/EFA; the question is whether the markets will obey or whether they simply will collapse.

Of note on the chart above:

- Prices have had a terrible time closing above the 20d MA. Until this occurs, the I-Fund is an avoid.

- We are nearing a relatively strong level of support. If we hold here, then it's possible that the worse has passed.

- If the upcoming level of support does not hold, expect another -3% drop in the I-Fund to the next possible support level.

The I-Fund gives us a view of what happens when prices do not behave the 200d MA and pierce through it, with falling 20d and 50d MAs above the prices. Recall from above, this is the exact situation we have for the S&P500, so this I-Fund/EFA chart could help you visualize what could go wrong with the S&P500.

Again, if you're in either the C-Fund/S&P500 or I-Fund/EAFE Index, you're taking a beating (but you probably already know this ... )

===================

S-Fund

The S-Fund is supposed to be the entire market without the S&P500. So, an equal-weighted investment in the S-Fund AND the C-Fund would represent two positions in the entire market.

The S-Fund is represented by the ETF VXF. It looks alot like the C-Fund, e.g., it has a solid avoid rating:

I didn't bother drawing support lines for the simple reason that you should be able to do this yourself.

Of interest on the graph above is:

- We are trading well below the 20d MA (Green) and the 50d MA (Blue).

- The 20d and 50d are in a downtrend, and are converging to the 200d MA (red)

- We've not yet hit the 200d MA in prices, nor have we tested the 200d MA.

- We're having a difficult time closing above the 20d. Until this occurs, we can't even consider entering the S-Fund.

===========================

Since our reallocation signal on June 6th the entire portfolio is up +0.279% with the 46% F-Fund / 54% G-Fund allocation. By reference, the C-Fund has fallen -1.259%, the I-Fund has fallen -3.805%, and the S-Fund has dropped -0.363%. The G-Fund, which is a cash fund, has increased +0.124%.

Since the index peak on 5/2/11, the 3 equity funds, if equal weighted (33% in C-Fund, 33% in I-Fund, 33% in S-Fund) have fallen -8.8%. We moved to CASH on 5/24, realizing a loss of -3.325%, gained +0.077% in the period 5/24 to 6/6, and as stated above, have incrementally added to our funds another +0.279%.

Market timing using trend following methods guarantees that you will always miss the top, and you'll always miss the bottom. The intent here is to ensure that you do not experience a melt down and ride the markets down, finally realizing that you made a mistake, selling at the bottom, and nervous to get back in.

====================

Remember, you are responsible for your own investment decisions, and I am not. Please do your diligence, and please take ownership for your actions.

Put a reminder on your calendar to check back in here the last two days of the month. We most likely will be reallocating funds at that time, to take advantage of the unused transfer remaining for the month of June.

Regards,

pgd

Monday, June 20, 2011

Update on TSP through June 17

There isn't much to report on. The present account has a mixture of G-Fund, which is the equivalent of cash, and F-Fund, which closely resembles the ETF: AGG. We moved long in the F-Fund on 6/6, and since then have introduced more volatility to the portfolio but not much gain. This being said, we're far better off than the folks who are still holding equity funds.

Since our signal date of 6/6 and through 6/17, the TSP has experienced the following:

G-Fund: increased +0.076% (I know, pennies)

F-Fund: increased +0.128%

C-Fund: decreased -1.040%

S-Fund: decreased -1.895%

I-Fund: decreased -3.049%

Since I recommended a move out of the C, S and I funds we all have been isolated from that downdraft.

Since 6/6 our portfolio has gained +0.100% with the ratio 46% in the F-Fund and 54% in the G-Fund. Not much, but then again, better than losing ground at this point in the markets.

At the present time I see nothing on the horizon indicating that we should not continue in the F-Fund. The C-Fund (mimics the S&P500) is clearly in cash. Ditto the I-Fund (mimics the ETF: EFA). The S-Fund, which mimics the ETF: VXF, is giving us mixed signals but given all of my other indicators, we'll stay out of this one too (no system is perfect).

We'll revisit near the end of the month so we can burn one of our remaining allocation changes if necessary to rebalance.

==================

Remember, you are responsible for your own investment decisions, and I am not. Please take ownership for your actions, and please do your diligence.

Regards,

pgd

Since our signal date of 6/6 and through 6/17, the TSP has experienced the following:

G-Fund: increased +0.076% (I know, pennies)

F-Fund: increased +0.128%

C-Fund: decreased -1.040%

S-Fund: decreased -1.895%

I-Fund: decreased -3.049%

Since I recommended a move out of the C, S and I funds we all have been isolated from that downdraft.

Since 6/6 our portfolio has gained +0.100% with the ratio 46% in the F-Fund and 54% in the G-Fund. Not much, but then again, better than losing ground at this point in the markets.

At the present time I see nothing on the horizon indicating that we should not continue in the F-Fund. The C-Fund (mimics the S&P500) is clearly in cash. Ditto the I-Fund (mimics the ETF: EFA). The S-Fund, which mimics the ETF: VXF, is giving us mixed signals but given all of my other indicators, we'll stay out of this one too (no system is perfect).

We'll revisit near the end of the month so we can burn one of our remaining allocation changes if necessary to rebalance.

==================

Remember, you are responsible for your own investment decisions, and I am not. Please take ownership for your actions, and please do your diligence.

Regards,

pgd

Monday, June 6, 2011

June 3 Weekend Update - Partial Move to F-Fund

.

Summary

We are nearing oversold levels, which means the equity markets could bounce here in the next week. Despite this possibility, I do not intend to move into the C-Fund, I-Fund, or S-Fund until we see some form of stabilization in the equity markets.

Regards,

pgd

Summary

- Overall, we're 100% in cash as of the 5/24 close

- The I-Fund and S-Fund have both indicated transactions back to LONG, but, with the C-Fund clearly in CASH, we will remain in CASH between the equity funds.

- The F-Fund, which is a bond fund, is indicating we should be long.

Conclusions: for the more aggressive, partial allocation in the F-Fund could be prudent.

========================

Interest rate risk (e.g., hikes), is relatively low due to the poor showing of the economy, specifically, last week's jobs reports. This means that bonds should continue to appreciate, and the general trend has been for yields to drop over the past month. While I typically do not allocate money to bonds when I can allocate to equities, since I'm in cash, I do have funds to play with.

Correspondingly, I'm moving 46% of the available funds to the F-Fund, which is a bond fund. The remaining 56% will remain in the G-Fund.

We are nearing oversold levels, which means the equity markets could bounce here in the next week. Despite this possibility, I do not intend to move into the C-Fund, I-Fund, or S-Fund until we see some form of stabilization in the equity markets.

Regards,

pgd

Tuesday, May 24, 2011

We're Moving to Cash

.

With the close of markets on May 23rd, the primary holding, C-Fund, has signaled a move to CASH. S-Fund is still LONG, and F-Fund is still LONG. Since the C-Fund is 97% of our holdings at the present time, I see no compelling reason to remain in any of the funds.

The problem here is that we have used our two transfers this month, so to be on the safe side, I'm moving 100% over to the G-Fund.

Today will most likely be an up day, so we will recover some of the losses incurred yesterday. Since my crystal ball is as good as yours, I wouldn't try to anticipate what the week holds; of course, you're in control of your own world.

Make your changes by 12:00 noon to have them effective at the close of business on May 24th.

==================

Remember, you are responsible for your own investment decisions, and I am not. Please do your own work, and please take ownership for your actions.

Regards,

pgd

With the close of markets on May 23rd, the primary holding, C-Fund, has signaled a move to CASH. S-Fund is still LONG, and F-Fund is still LONG. Since the C-Fund is 97% of our holdings at the present time, I see no compelling reason to remain in any of the funds.

The problem here is that we have used our two transfers this month, so to be on the safe side, I'm moving 100% over to the G-Fund.

Today will most likely be an up day, so we will recover some of the losses incurred yesterday. Since my crystal ball is as good as yours, I wouldn't try to anticipate what the week holds; of course, you're in control of your own world.

Make your changes by 12:00 noon to have them effective at the close of business on May 24th.

==================

Remember, you are responsible for your own investment decisions, and I am not. Please do your own work, and please take ownership for your actions.

Regards,

pgd

Monday, May 23, 2011

Weekend Update for May 20

.

In a nutshell, no changes.

Had we done equal-weighting into the TSP funds on this last allocation (equal weight assigns equal portions to the available funds and is recommended by many financial advisors for "diversification"), we would have experienced the following changes in the specific funds:

F-Fund: +0.796%

C-Fund: -1.971%

I-Fund: -5.833%

S-Fund: -2.59%

Ouch.

As it turns out, we're getting beat up, but here's our realized performance since the signal on 5/2:

In a nutshell, no changes.

Had we done equal-weighting into the TSP funds on this last allocation (equal weight assigns equal portions to the available funds and is recommended by many financial advisors for "diversification"), we would have experienced the following changes in the specific funds:

F-Fund: +0.796%

C-Fund: -1.971%

I-Fund: -5.833%

S-Fund: -2.59%

Ouch.

As it turns out, we're getting beat up, but here's our realized performance since the signal on 5/2:

F-Fund: +0.008%

C-Fund: -1.912%

I-Fund: 0%

S-Fund: -0.052%

I chose this allocation simply because of the desire to reduce volatility in the present market, and because I was anticipating a growth in volatility, which makes everybody nervous.

Note that the timer has the I-Fund in CASH. You absolutely should NOT be in the I-Fund at this time.

=====================

Staying the Course

I'm getting asked about why we're in the market right now if we're down 2%?

Well:

- The adaptive timers have only fired the I-Fund as CASH, all the others are still LONG.

- 2% drop in equity is not a great deal of drop. Historically, my timer system has dropped me nearly 10% in this portfolio. If this gives you heartburn then you should simply increase your ratio into the G-Fund

- Volatility, while increasing, isn't indicating a terrible breakdown in the markets. We should continue to march along nicely here.

As evidence of 3) take a look at the following chart:

I've presented this chart in previous write-ups so you can look back and read about it. Bottom line, anticipated longer-term volatility (as measured by the ETF VXZ) compared to the next 30d anticipated short-term volatility (as measured by VXX) is still well above the 7w trend line, and although the trend line is falling, we're still above it, and this is still indicative of a bullish market.

Stay the course.

Current plans are to reallocate on May 31st if we don't get moved to cash prior to that date.

=================

Remember, you are responsible for your own investment decisions, and I am not. Please do your diligence, take ownership for your actions, and understand that nobody can predict the future.

Regards,

pgd

Thursday, May 19, 2011

I-Fund Confirms CASH, but We Are Not In This Fund, So No Worries ...

.

I run two independent models for the GGT-TSP portfolio. One of them is an adaptive timer that uses the daily change in the funds to help determine what to do the next day, and another is based purely on moving averages, specifically moving average crossings and slopes.

With the close of 5/19, the I-Fund has confirmed using both methods that you should not be in the market in this fund. The I-Fund is in CASH.

There is no question, the C-Fund, which tracks the S&P500, and the S-Fund, which tracks the market ex-S&P500, are both experiencing tremendous pressure to the downside. It's important to note that neither the C-Fund nor the S-Fund are signalling a move to CASH. What is important with these two is that

I run two independent models for the GGT-TSP portfolio. One of them is an adaptive timer that uses the daily change in the funds to help determine what to do the next day, and another is based purely on moving averages, specifically moving average crossings and slopes.

With the close of 5/19, the I-Fund has confirmed using both methods that you should not be in the market in this fund. The I-Fund is in CASH.

There is no question, the C-Fund, which tracks the S&P500, and the S-Fund, which tracks the market ex-S&P500, are both experiencing tremendous pressure to the downside. It's important to note that neither the C-Fund nor the S-Fund are signalling a move to CASH. What is important with these two is that

- the slopes, which indicate $/day gain, are still positive. On a 65-day basis, the S&P500 is in an uptrend,

- the 5d and 65d moving averages are still bullish, e.g., the 5d > 65. These are in a long-term uptrend.

What is problematic is that both of these funds are within a whisker of moving to CASH. A whisker.

What is further problematic is that we only have one more transfer to accomplish for the month (we are allowed 2 transfers per month), and we have 98% in the S&P500 fund, 2% in the ex-S&P500, and 1% in the 2-5 year bond fund.

==================

Here is my plan for going forward: stay the course in the C-Fund, S-Fund, and F-Fund. No changes.

This could certainly change with Friday's close, Monday's, or Tuesday's. Your crystal ball is as good as mine.

Relax folks. Yes, we're down -1.1% since our entry. It may go down more, it may go up. If you're still working and contributing to your TSP, then you are accumulating shares a bit cheaper than if you were in cash. This is good, if we believe that in the future the markets will go up. I believe that they will. If you are retired, then you certainly can go to cash and nobody would fault you. Your risk tolerance decides your course from here.

===================

Remember, you are responsible for your own investment decisions, and I am not. Please do your own diligence, and please take ownership for your actions.

Regards,

pgd

Monday, May 9, 2011

May 6 Weekend Update - Volatility as an Indicator

.

Summary

Summary

- Stay the course for now. None of the TSP funds are indicating a move to cash, but yes, they are pulling back somewhat. Let the markets decide what we should do, do not try to anticipate.

- Since I went long on 5/2, my account has dropped a total of -1.565%. By reference, the C-Fund has dropped -1.526%, the S-Fund has dropped -2.222%, and the I-Fund has dropped -3.748%. The F-Fund, which is a bond fund, has increased +0.528% in this time.

- The present allocation of 97% C-Fund, 1% F-Fund, and 2% S-Fund is keeping us in the most stable portfolio combination as of May 6. Any deviation from this portfolio will introduce more volatility at a greater rate than recent gains (taking more risk for the same or less gains, not advised).

- For the record, the 12-month personal rate of return on this portfolio is 10.38%. Note that this includes the period 4/22/10 to 9/7/10, where I sat the market out in cash due to taking some time off. Drawdown has been low single digits over the past year, yielding a Calmar Ratio of just over 3.0.

==================

Volatility as an Indicator

Volatility is a measure of how much a stock moves in a given time frame. It's a squirrelly beast when it comes to the markets, because future volatility over the next 30 days and beyond has a big influence on option prices, and correspondingly, to money flow within the markets.

The ETF VXX gives a reasonable view of volatility as reported in the market. I say "reasonable", because it's not a perfect match. The Yahoo! symbol ^VIX is the CBOE index for volatility for the next 30 days, but we can't trade it directly. VXX is the closest ETF to "the VIX", with a coefficient of regression of 0.82 (R^2 = 1.00 = perfectly correlated). VXZ is related to "the VIX" in that it is a tradeable instrument that is an estimate of volatility beyond 30 days.

For the last several weeks, the VIX has been really low, as in multi-year lows. This means that folks think that the markets are going to hum along nicely with low volatility. Correspondingly, VXX and VXZ have been very low too.

When the markets begin to jump around, VXX moves faster than VXZ. The two are close (R^2 = 0.93), but VXX jumps faster. This allows us to compare the two, and when we do, we get a view of the market in general.

Take a look at the following picture:

This picture is available here; you can bookmark the link.

What is shown in the lower graph is the ratio of VXZ (longer-term expected volatility) divided by VXX (shorter-term expected volatility). The scale is a weekly scale. The blue line is a 7-week moving average.

When the bars are trading below the blue line we can expect rougher roads ahead. Right now the most recent week saw a drop, but not a penetration below the blue line. This is bullish overall.

When the blue line is pointing upward, we typically can expect the markets to move upward. The eye has a hard time discerning this, so I included a slope line at the top of the graph. The slope line tells us with more detail about what the ratio VXZ:VXX is doing.

Right now, the slope is positive at +0.06 -- VXZ is growing faster than VXX, -- OR -- VXX is getting smaller at a faster rate than VXZ. Either way, the markets are still in an up trend, as far as FUTURE expectations are concerned.

The dropping VXZ:VXX ratio simply means that we are slowing -- but because the value is positive at +0.06, we are still in an up trend.

We can still move upward in the markets if the slope line is pointing downward. The key aspect is whether the slope line has a positive value -- it is presently +0.06 -- or if it has a negative value. It should be clear that once the VXZ:VXX ratio crosses below the 7w average line, OR the slope line turns negative, that we should be out of the markets.

Until then, stay the course. Remember though, your crystal ball is as good as mine.

Check this chart as time allows -- use the link provided above.

=============================

Remember, you are responsible for your own investment decisions, and I am not. Please do your own diligence, and please take ownership for your actions.

Regards,

pgd

Monday, May 2, 2011

Moving Long as of Monday, May 2nd

.

A series of unfortunate events occurred last Thursday/Friday which precluded my ability to review the TSP funds at the critical end-of-month time frame. Given this, we'll move long today.

===================

Summary

===================

TSP Review

With some frustration, the news from Bernanke last Wednesday caused my latest move-to-cash signal to whipsaw, and with Thursday's action, we had a confirmed LONG call across the board. I missed this signal on Thursday/Friday due to events beyond my control, and the weekend review has caught the change in signal.

Allocation into the funds begins with a 100d lookback on daily price changes. I use the actual TSP fund prices, not ETFs. One aspect I am concerned about is risk -- "sell in May and go away" comes to mind, so an analysis of marginal risk contribution is required.

Marginal risk contribution is the anticipated change in volatility if we start with an index (in this case, the S&P500), and then add 1% (arbitrary) of Fund X to the portfolio. The difference in volatility is useful because we can see what the impact of adding each fund will be to daily swings in value, averaged over 100 days:

Here's the results:

A series of unfortunate events occurred last Thursday/Friday which precluded my ability to review the TSP funds at the critical end-of-month time frame. Given this, we'll move long today.

===================

Summary

- New Allocation as of close on Monday, May 2nd:

C-Fund: 97%

S-Fund: 2%

F-Fund: 1%

- Make the allocation switch by 12:00 EST to be effective 5/2.

===================

TSP Review

With some frustration, the news from Bernanke last Wednesday caused my latest move-to-cash signal to whipsaw, and with Thursday's action, we had a confirmed LONG call across the board. I missed this signal on Thursday/Friday due to events beyond my control, and the weekend review has caught the change in signal.

Allocation into the funds begins with a 100d lookback on daily price changes. I use the actual TSP fund prices, not ETFs. One aspect I am concerned about is risk -- "sell in May and go away" comes to mind, so an analysis of marginal risk contribution is required.

Marginal risk contribution is the anticipated change in volatility if we start with an index (in this case, the S&P500), and then add 1% (arbitrary) of Fund X to the portfolio. The difference in volatility is useful because we can see what the impact of adding each fund will be to daily swings in value, averaged over 100 days:

Here's the results:

- I-Fund: +0.141%/day

- S-Fund: +0.112%/day

- C-Fund: +0.095%/day

- F-Fund: +0.002%/day

As a reference, the S&P500 has a volatility of +0.101/day over the last 100 days.

These results show us that the I-Fund has been extremely volatile as of late, and addition of shares of the I-Fund and S-Fund, because they have an above-average volatility compared to the S&P500, need to be weighed in terms of their returns.

The Sharpe Ratio is a good way to value this, simply because we now know the volatility, and simply need to calculate the returns over the past 100 days. Doing so produces the following Sharpe Ratios, using a risk-free investment of 0.25% annualized:

- I-Fund: 1.96

- S-Fund: 2.14

- C-Fund: 2.20

- F-Fund: 0.18

What these results tell me is that by-and-large, the C-Fund is the best candidate for the majority of our funds, as it has the greatest reward/risk ratio over the past 100 days. Furthermore, the S-Fund comes in a close second, so some portion of the portfolio should most likely contain the S-Fund. The fact that the F-Fund is well under the rest of the funds simply tells me that

Through the magic of math, it's possible to find the combination that produces the best reward/risk ratio of the portfolio above. Surprisingly, I-Fund lands a big, fat goose-egg in terms of allocation -- 0%. This tells me that the marginal contribution of 1% of I-Fund is worse than the combination of some form of S-Fund and F-Fund, hence, we have the stated allocations above.

Here's the target Efficient Frontier, as I know many of you are interested:

From the picture above you can see where the four funds lie on the "perfect" solution curve -- the blue curve.

For you more aggressive, the I-Fund is sitting PERFECTLY on the curve -- but the higher reward is offset by far more risk -- see how far the I-Fund is deviating from the red line? This means that if you invest in the I-Fund, you are taking on a disproportionate amount of risk, e.g., risk is growing faster than gain. This is bad.

At the end of the day, I've selected the allocations shown above:

- C-Fund: 97%

- S-Fund: 2%

- F-Fund: 1%

I don't normally invest in the F-Fund but I think bond yields will be stable here for the next month or so, resulting in an ability to offset the volatility in the S-Fund but still see some upside. Note that over the past 100 days that the F-Fund has a 0.8% gain, so it is somewhat positively correlated with the markets (which is rare in general).

======================

Remember, you are responsible for your own investment decisions, and I am not. Please do your diligence, and please take ownership for your actions.

Regards,

pgd

Wednesday, April 20, 2011

GGT Risk Model Signals a Complete Transfer to CASH

.

Summary

TSP Status

With the close of markets on 4/19/11, the GGT risk model has indicated that the C-Fund should be liquidated to cash. This is presently 98% of my holdings.

The natural question is now one of re-allocation between the remaining funds: F-Fund, I-Fund, and S-Fund. To answer this, it is important to understand where we are.

The graph above shows the return/volatility universe for the 3 equity funds available within TSP. Actual TSP data is used, e.g., proxy ETFs data was NOT used. The blue curve represents all the different combinations of C-Fund, S-Fund, and I-Fund that we can achieve within our portfolio. The unlabeled yellow diamond, located on the blue curve between C-Fund and S-Fund, is where we are today with our present portfolio. Note that the F-Fund is on the bottom of the figure, with an annualized return of less than 0%.

The analysis starts simply by asking the question "what combination moves us up greater than the return of where we are but does so at lower risk? We are already at 98% C-Fund, 1% in each of the S-Funds and I-Funds.

The math is complicated but there is no way to get greater projected return at lower risk than where we are today. This is because we are presently sitting on the blue curve -- we already have a portfolio that is extremely efficient.

The next part of the analysis looks at an adaptive moving average of each of the prices of the C-Fund, I-Fund, S-Fund, and F-Fund. When prices are below the moving average, we should sell. When prices are above the moving average, we should be long. It's a simple system and does not issue changes all that often (e.g., the C-Fund only offered 5 signals to move to CASH in the last 365 calendar days).

Right now the C-Fund has issued a signal to move to CASH, and this is confirmed for two consecutive days. The I-Fund and S-Fund are still long.

Strategy

The TSP funds offer the ability to exchange only 2x per month. This signal today will be 1 of those 2 exchanges.

I fully intend to move the C-Fund to cash. I will place the order at www.tsp.gov before noon EDT so that it is effective today.

The question now is what to do with the I-Fund and S-Fund allocations of 1% each.

In the risk-adjusted model, and with an eye towards the figure above, you can see that the I-Fund has greater volatility but has lower return over the past 100 days, when compared to the S-Fund. The calculations (not presented here) for allocation to the I-Fund ZERO any allocation in the I-Fund, as the volatility is increasing and return is decreasing. This is bad for our portfolio. This forces me to conclude that the money in the I-Fund will be moved to CASH.

This leaves 1% in the S-Fund. The risk-adjusted model actually indicates leaving this 1% intact, as a 100% allocation in the S-Fund falls directly on the blue-curve. 99% in cash simply lowers our risk of being in the S-Fund by .... wait for it ... 99%. Bottom line, if you want to leave some money in the S-Fund go ahead, but to align with the model, you probably should not have much in there at all (e.g., no more than 1%).

I personally intend to move 100% of everything to the G-Fund, which is CASH. No sense worrying about the 1%.

=================

Performance

The rolling, day-for-day 12-month realized performance of this strategy is 10.16%, as measured by www.tsp.gov. The drawdown, or the maximum value attained in equity to the lowest point since the peak is -1.1%. This gives me a reward/risk ratio of 9.24, and anything over 3.0 is considered outstanding. There is virtually no ulcer index with this strategy, which means I sleep well at night.

Since my last long signal on 3/28/11, I have realized the following performance with my stated allocations:

Summary

- In intend to move 100% of my wife's funds to CASH, effective with the close today. New contribution allocations will be 100% into CASH.

===================

TSP Status

With the close of markets on 4/19/11, the GGT risk model has indicated that the C-Fund should be liquidated to cash. This is presently 98% of my holdings.

The natural question is now one of re-allocation between the remaining funds: F-Fund, I-Fund, and S-Fund. To answer this, it is important to understand where we are.

The graph above shows the return/volatility universe for the 3 equity funds available within TSP. Actual TSP data is used, e.g., proxy ETFs data was NOT used. The blue curve represents all the different combinations of C-Fund, S-Fund, and I-Fund that we can achieve within our portfolio. The unlabeled yellow diamond, located on the blue curve between C-Fund and S-Fund, is where we are today with our present portfolio. Note that the F-Fund is on the bottom of the figure, with an annualized return of less than 0%.

The analysis starts simply by asking the question "what combination moves us up greater than the return of where we are but does so at lower risk? We are already at 98% C-Fund, 1% in each of the S-Funds and I-Funds.

The math is complicated but there is no way to get greater projected return at lower risk than where we are today. This is because we are presently sitting on the blue curve -- we already have a portfolio that is extremely efficient.

The next part of the analysis looks at an adaptive moving average of each of the prices of the C-Fund, I-Fund, S-Fund, and F-Fund. When prices are below the moving average, we should sell. When prices are above the moving average, we should be long. It's a simple system and does not issue changes all that often (e.g., the C-Fund only offered 5 signals to move to CASH in the last 365 calendar days).

Right now the C-Fund has issued a signal to move to CASH, and this is confirmed for two consecutive days. The I-Fund and S-Fund are still long.

Strategy

The TSP funds offer the ability to exchange only 2x per month. This signal today will be 1 of those 2 exchanges.

I fully intend to move the C-Fund to cash. I will place the order at www.tsp.gov before noon EDT so that it is effective today.

The question now is what to do with the I-Fund and S-Fund allocations of 1% each.

In the risk-adjusted model, and with an eye towards the figure above, you can see that the I-Fund has greater volatility but has lower return over the past 100 days, when compared to the S-Fund. The calculations (not presented here) for allocation to the I-Fund ZERO any allocation in the I-Fund, as the volatility is increasing and return is decreasing. This is bad for our portfolio. This forces me to conclude that the money in the I-Fund will be moved to CASH.

This leaves 1% in the S-Fund. The risk-adjusted model actually indicates leaving this 1% intact, as a 100% allocation in the S-Fund falls directly on the blue-curve. 99% in cash simply lowers our risk of being in the S-Fund by .... wait for it ... 99%. Bottom line, if you want to leave some money in the S-Fund go ahead, but to align with the model, you probably should not have much in there at all (e.g., no more than 1%).

I personally intend to move 100% of everything to the G-Fund, which is CASH. No sense worrying about the 1%.

=================

Performance

The rolling, day-for-day 12-month realized performance of this strategy is 10.16%, as measured by www.tsp.gov. The drawdown, or the maximum value attained in equity to the lowest point since the peak is -1.1%. This gives me a reward/risk ratio of 9.24, and anything over 3.0 is considered outstanding. There is virtually no ulcer index with this strategy, which means I sleep well at night.

Since my last long signal on 3/28/11, I have realized the following performance with my stated allocations:

- close of 4/19/11: gain of +0.302%

- total trading days of signal: 17

- maximum equity peak during 3/28 - 4/19: +2.04% on 4/6

- maximum equity dip during 3/28 - 4/19: -0.269% on 4/18

- if 100% invested in G-Fund during same period: +0.183%

Overall, this isn't a great performance -- the risk-free approach is nearly the same as my achieved gain. I do note that in terms of daily change of the portfolio that we have the following averages over the last 17 trading days:

- G-Fund: +0.011%/day

- F-Fund: -0.052%/day

- C-Fund: +0.019%/day

- S-Fund: +0.041%/day

- I-Fund: +0.032%/day

- 98% C-Fund, 1% S-Fund, 1% I-Fund: 0.000%/day

I achieved virtually no volatility over the past 17 trading days, which is what I desire to do with this portfolio. This is what the Efficient Frontier methodology does for me. The cost is not participating in the highest gains at a disproportionate risk level, but I sleep well.

Markets will most likely be up today, so I will most likely finish well above the +0.302% level, handedly beating the risk-free return of the G-Fund. It doesn't always work out this way though.

==================

Remember, you are responsible for your own trading decisions, and I am not. Please do your diligence, and please take ownership for your actions.

Regards,

pgd

Friday, April 15, 2011

Stay the Course on the Long Side

.

A question came in over night about "selling the bounces" and my short answer is that there is nothing in the TSP adaptive routines for the C-Fund, S-Fund, or I-Fund that indicates that I should move to cash.

Since my long signal on March 28 I have the following performance, with the suggested allocations:

A question came in over night about "selling the bounces" and my short answer is that there is nothing in the TSP adaptive routines for the C-Fund, S-Fund, or I-Fund that indicates that I should move to cash.

Since my long signal on March 28 I have the following performance, with the suggested allocations:

- C-Fund, 98% allocation, +0.429% gain

- I-Fund, 1% allocation, +0.023% gain

- S-Fund, 1% allocation, +0.009% gain

This configuration continues to exhibit the best return/risk allocations given the previous 100 days of volatility. Yes, the I-Fund is up +2.313% since the signal, but the volatility swings are greater than 1.4% per day on average, and volatility is increasing, so my suggestion is to keep the suggested allocations (for now).

I'm sitting pat, but of course, my crystal ball is as good as yours. This could all change with today's action.

==================

Regards,

pgd

Sunday, April 10, 2011

Adaptive Timer Signals CASH on F-Fund

.

Summary

Summary

- We are presently 100% LONG in the portfolio in the C-Fund, S-Fund, and I-Fund. Gain since the last signal (March 28), at the target percentages, is +1.492%. We peaked at a gain of 2.042% this past Wednesday, so we have given up -0.55%. Contrasting, the S-Fund peaked at 3.677% and has dropped to 2.353%, a loss of -1.324%, and the I-Fund peaked Friday at 3.201%. Note that these are weighted performance values, e.g., with the allocations in the next bullet.

- Our portfolio allocations are 98% in the C-Fund, with 1% in the I- and S-Funds. The allocation represents the best reward/risk on a short-term basis, and you see this volatility above in the 1st bullet.

- The F-Fund has signaled a move to CASH. You probably do not want any money in the F-Fund right now, and I never put any there.

- While there are signs of a topping market, I see no compelling reason to move anything to cash. If you're nervous, then go ahead, but for my particular circumstance, I'm sitting pat.

==============

Relative Market Volatility

I've presented the following graph numerous times over the last months -- it gives us a good view of the market as a whole in terms of volatility. Generally, when short-term volatility is low, the VXX has a lower number than the longer-term VXZ, and the ratio rises. A dropping VXX generally corresponds to an increasing market, in general.

The top graph is the SLOPE of the weekly moving average of the ratio VXZ to the VXX (these are ETFs -- look them up here to learn more about these specific entities). The important thing is that the slope is positive AND it's pointing upward. This really is all that you need to know. If you want to bookmark this chart, here's the link.

The bottom graph is the ratio of the longer-termed volatility ETF VXZ to the shorter-termed volatility ETF VXX. We see that the ratio has closed for 3 weeks above the 7w moving average, which I consider bullish for holding our funds.

Of course, this makes no representation as to what the following week will hold. The markets could collapse, or they could move higher -- your crystal ball is as good as mine. All I can say is that as of this writing that we need to be in the markets, and based on signals the last week of the month -- we are.

================

New CASH signal on F-Fund

I personally do not trade the F-Fund, but I track it. As of the close of business Wednesday, April 6th, the GGT Adaptive Timer signaled a move to CASH for the F-Fund. Note that this is calculated using the actual prices for the F-Fund, not on the ETF proxy that I sometimes use, AGG.

If you are trading this fund, and again, I don't, but if YOU are, it probably is prudent to move to CASH. The earliest you could have moved would have been Thursday night, and Friday's close was 0.9997 of Thursday's close, e.g., the same value for all intensive purposes. Since our signal on March 28th the F-Fund has DROPPED -0.254%, but allocations were 0%, so if you had listened to me, you'd resisted any temptation to put money in the F-Fund. :o) -0.254% may not sound like a lot, but on $100K it's $254, which is a large number of Starbucks venti lattes.

================

Remember, you are responsible for your own trading decisions, and I am not. Please do your own diligence, and please take ownership for your actions.

Regards,

pgd

Sunday, March 27, 2011

Confirmed Signal LONG for Monday, March 28

.

Summary

Summary

- Volatility indicators are showing that we are early, but that the bulls are more powerful over the past week.

- The TSP / GGT Adaptive Timer, which uses the raw price signals from www.tsp.gov in the calculations, has all holdings LONG.

- The historical GGT timer has the VXF (proxy for the S-Fund) LONG, but the EFA (I-Fund) and SPY (C-Fund) are still in CASH.

- For Monday, March 28th, the GGT TSP portfolio will be transitioning LONG. This is an aggressive move, as not all timer methods are indicating that this is a good choice.

============

Volatility

Perceived volatility in the market, as measured by the ratio of the longer-termed anticipated volatility VXZ compared to the shorter-termed 30-day anticipated volatility VXX, has improved. Here's the chart:

As with all my charts, right-click on it to open in a new window or tab.

In the chart above, which is linked here, we have the ratio of longer-termed volatility to that of short-termed volatility. Increasing values of this ratio are considered shorter-termed bullish, and this is what the past week has delivered.

As you can see in the chart above, the ratio of VXZ:VXX has closed above the 7w moving average for the first time since the 2nd week of February, giving us reason to believe that we may be moving upward from here as far as the broad markets are concerned. Because I have no knowledge of the right side of the graph for the next couple of weeks, we must take this preliminary signal as bullish for the market in general.

I note with some caution that this 7-week line will be tested going forward. Observe the May-June 2009 sequence, where the 7-week line was penetrated or tested for nearly 8 weeks. During this time you may recall that it was difficult to make money in the TSP funds. Note though that the slope of the 7w line never went below 0, so we had confirming indications to remain long during this test/penetration of the 7w line.