With the close of markets on Friday, May 4th, the GGT/TSP model has signaled that we should close all positions and move to a combination of G-Fund and F-Fund. I simply think bond-risk isn't worth the trouble, so I'm moving everything to G-Fund for now.

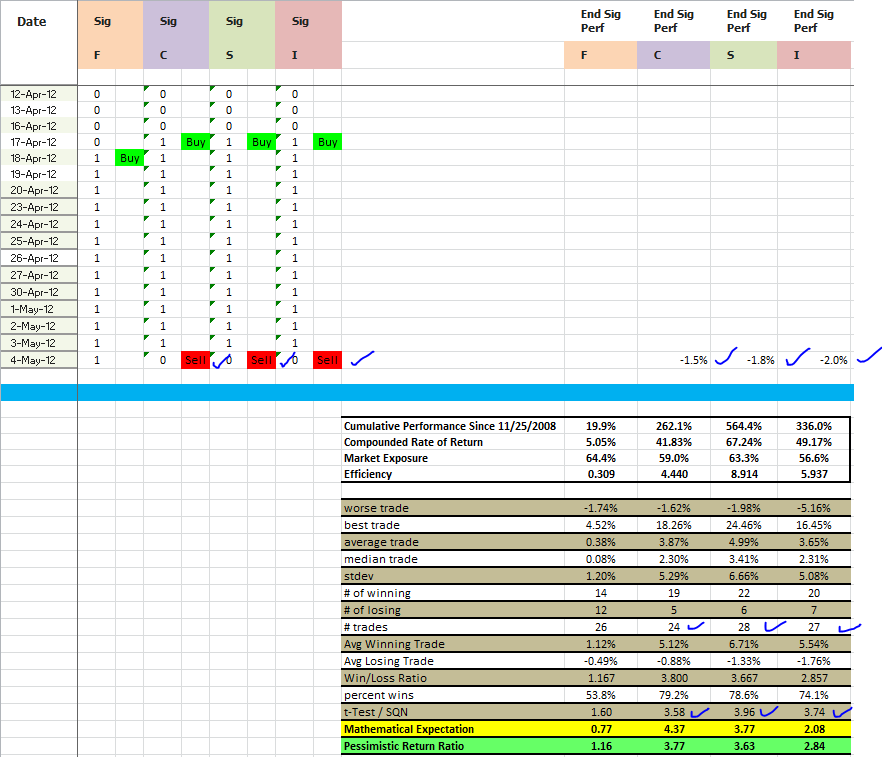

As you can see in the upper right area, this last sequence since the last buy signal has not been positive. The actual amount lost will be a function of Monday's behavior -- if it's up the losses will be slightly less than shown, if Monday's markets are down we will record a greater loss.

The table shows that over the long haul, e.g., since 11/25/08, the model has been quite productive and accurate. This is my "new" model which I recently improved (substantially) from the previous one which missed the December/January signals. This model also has a different set of metrics which are independent, so I can watch behavior on multiple inputs and ensure that we're behaving the way we expect to. To date I have not been able to develop an independent model which outperforms the statistics above.

The F-Fund, which is a bond fund, has the "worse" performance overall and is shown on the left of the table stats. The model's signalling engine is based in stocks, not in bonds, and it goes to reason that timing bonds with stocks is probably not a good thing in the long haul. Before we discount the F-Fund all together, note that overall, it does perform "okay" for a bond (low-volatility, low risk) vehicle, so it can play a role in our strategy if we decide it should. Note that I personally do not use the F-Fund in my allocations, as I am an aggressive investor.

The C-, S-, and I-Fund statistics are all quite compelling. The Compounded Rates of Return (CRR) for the three range from 41% to 67% over the past 3.5 years. The model has us invested between 56% and 63% of the time to produce those returns, so you can see that it is quite efficient (keep our powder dry when the model says to stay away).

Although equity and gains are what we bank and what we retire on, equity/gains are not the entire picture. The 3 metrics at the bottom: t-Test/SQN, Mathematical Expectation (ME), and Pessimistic Return Ratio (PRR) are all methods to quantify the robustness of the model, and they specifically check to ensure that the model does not lock in big losses relative to the wins it captures, and it rewards a greater number of trades, such that the more consistent the trades over time, the better the metrics.

t-Test/SQN is a methodology developed by Van K. Thorp and basically tests whether we are outperforming the null hypothesis, e.g. are we better than chance. From an empirical viewpoint, we want this value to be above 1.7 with the number of trades well above 20-30, but with a model such as ours (restricted to 2 trades / month), it will take some time to develop numbers way above 20-30. As you can see the number of trades in the C-, S-, and I-Funds are in the 24 - 28 range, which is just becoming statistically significant.

Mathematical Expectation is the "edge" of the system. In Vegas, the edge for the House is generally positive with all games except video poker, which is a loss-leader to get you deeper into the casino. This means that when you throw lots of people with money at their games, they will win in the long haul. ME values need to be positive for any system over the long haul, and values above 0.5 or so are good systems. Dr. Diliddo of VectorVest fame regularly produces ME values in the 0.3 - 0.8 range on portfolios that return a positive CRR over a year, so we don't need values as high as shown. I've rechecked the math and the values shown are not in error -- the TSP model produces very good results consistently, and consistency is rewarded in higher ME values.

Pessimistic Return Ratio (PRR) is also the "edge" of the system, but calculated very differently than T-Test or ME. If we had an infinite number of trades (we won't live long enough), the PRR will converge on a number called the Profit Factor, which you will find in many brokerage reports on your trading performance. Profit factor completely falls apart if the number of trades is low, hence, PRR is better because it considers the number of trades in the system AND it weights wins/losses accordingly. We want values above 1.0 here and values above 2.0 - 2.5 are considered good systems. We want the number of trades to be larger than 24 when looking at PRR, and you can see that we just hit that threshold with the C-Fund.

In the end, I'm moving my funds to cash, effective with the close of markets on Monday, May 7th.

Regards,

pgd